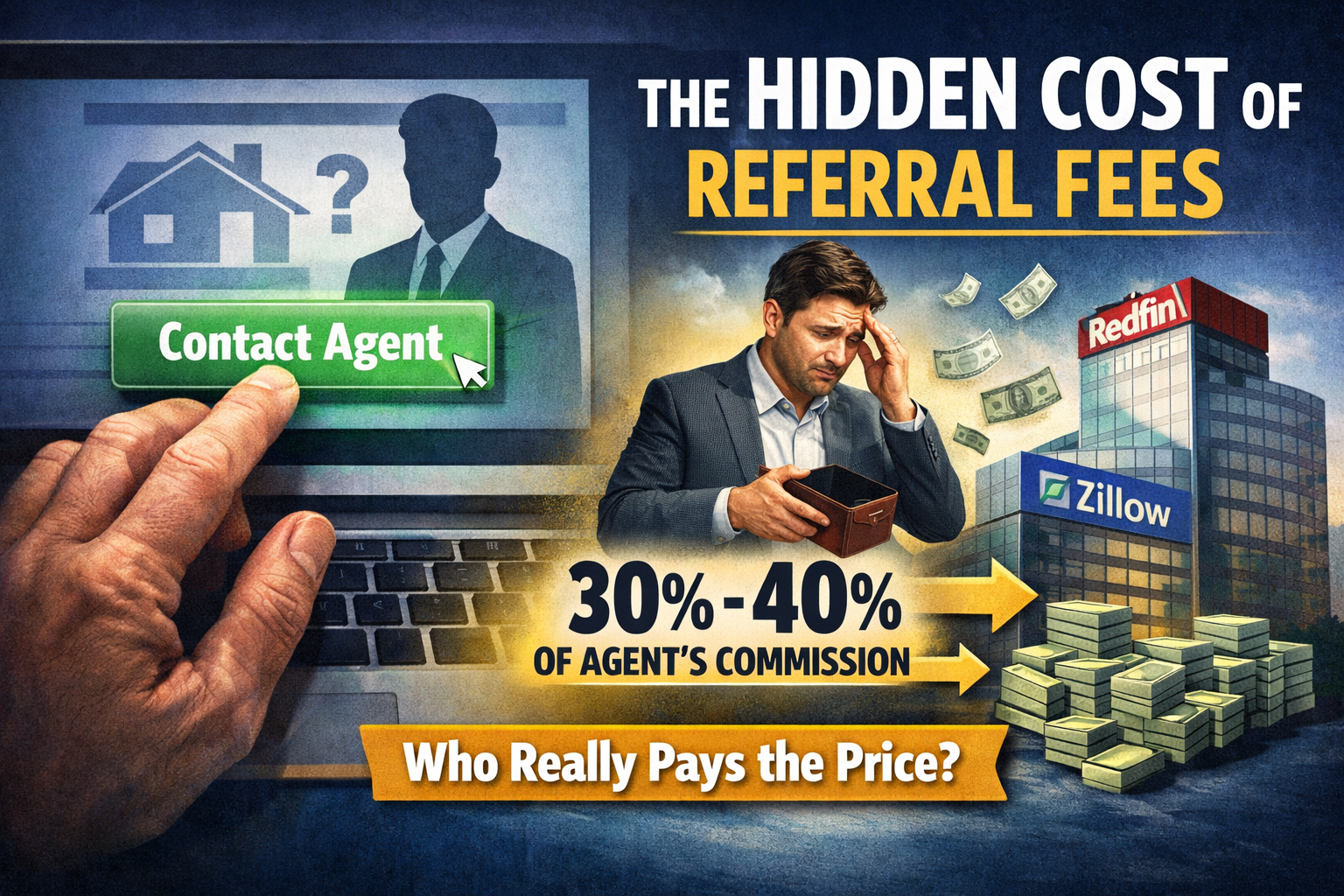

If you’re a homebuyer, there’s a good chance you’ve clicked “Contact Agent” on a portal and assumed you were simply being connected to a local professional. What many consumers don’t realize is that behind that click, there is often a 30% to 40% referral fee being paid out of the agent’s commission.

According to a February 2026 report from the Consumer Policy Center titled Commission-Based Home Referral Services: Consumer Impacts and Proposed Reforms , these referral fees have become a major revenue source for portals and referral platforms. In many cases, the buyer’s agent is paying 30% to 40% of their commission to the company that supplied the lead. Zillow, for example, commonly charges 40% on many transactions. Redfin’s partner fees range into the 30% to 40% range as well.

That money does not come from nowhere.

When an agent gives up 40% of a 3% commission, and then splits what’s left with their broker, the agent may net close to 1% or less. That creates pressure. The report argues that agents paying high referral fees are less likely to negotiate commissions downward. In a recent survey cited in the report, 55% of Americans said a 40% referral fee would tend to increase the commission paid by buyers.

For consumers, the issue is not simply the existence of referral fees. Referrals between agents have always been part of the business. The concern is transparency and incentives.

The report raises several practical risks buyers should at least be aware of:

• Agents may be selected based on conversion rates and speed, not necessarily fit.

• Large teams are often favored because they can respond instantly and handle volume.

• Some referral companies have affiliated mortgage or ancillary service relationships, which can create additional steering concerns.

• In many cases, buyers are not clearly told that the agent they are connected to is paying a significant referral fee.

From the agent side, this is not a simple black-and-white issue. Many agents participate because client acquisition is hard. The industry has roughly two million agents competing for about four million annual home sales. Lead flow matters. Paying 30% to 40% only when a deal closes feels safer than paying fixed monthly marketing fees with no guarantee of results.

But the long-term question is whether this model reinforces high commission structures at a time when consumers and regulators are scrutinizing compensation more closely than ever.

Legal pressure is already building. The report references class action litigation questioning whether these referral arrangements and disclosures meet fiduciary standards. State regulators are also being pushed to require clearer disclosure of referral fees upfront.

For consumers, the takeaway is simple: ask. If you are working with an agent you were connected to through a portal or referral platform, ask whether a referral fee is being paid and how much. It is a fair question.

For agents and brokers, the takeaway is just as clear. Transparency is no longer optional. Whether mandated by regulation or demanded by consumers, disclosure of referral fees is likely to become standard practice.

Referral fees are not new. What is new is the spotlight. And when 30% to 40% of a commission is being redirected before the agent even pays their broker, both consumers and professionals should understand how that affects pricing, service, and incentives.

The industry is changing. The agents who adapt with clarity and transparency will be the ones who thrive.